New Markets Tax Credit Overview

The New Markets Tax Credit (“NMTC”) Program was enacted in December 2000 as part of the Community Renewal Tax Relief Act of 2000. The goal of the NMTC Program is to increase investment in low-income communities throughout the country.

- The NMTC program is administered by the Community Development Financial Institutions Fund (“CDFI Fund”), an arm of the U.S. Treasury Department.

- Entities that have received a community development entity (“CDE”) designation by the CDFI Fund are eligible to apply for NMTCs.

- NMTCs are allocated annually by the CDFI Fund to CDEs under a competitive application process.

- The CDFI Fund has been authorized to award $33 billion of NMTC allocation (including 2011). To date, it has awarded $29.5 billion in allocation to CDEs. The amount allocated per year has varied between $2.5 billion to $5 billion.

Types of Projects that Qualify

- Commercial Real-Estate Development or Rehabilitation;

- Community Facilities/Non-Profit Facilities

- Office Real-Estate Development or Rehabilitation;

- Industrial Real-Estate Development or Rehabilitation;

- Mixed-Use Real-Estate Developments or Rehabilitation;

- Skilled Nursing and Assisted Living Developments or Rehabilitation;

- Hotel Developments or Rehabilitation;

- Businesses of Most Types;

- Not-For-Profit Entities.

New Markets Tax Credit Transaction Qualification

The NMTC program is designed to incentivize private capital to invest into low income communities for the purpose of creating an economic stimulus for these targeted communities. To achieve the program’s goal, a NMTC loan provides subsidized financing targeting operating businesses, value-add real estate transactions, and projects that provide services to low income persons. By design, NMTC program qualification is both objective by location and subjective based on the level of economic stimulus and community benefits the project will provide to the low income community as determined by the CDE.

Qualification by Location

The property or qualifying business must be located in a low income census tract based on year 2000 census data or have the primary objective of providing services to low income persons. A qualifying census tract is defined for the purposes of this program as having either: (a) a poverty rate of at least 20% or (b) a median income no more than 80% of area median income. Furthermore, most CDE programs require the property or qualifying business to be located in a census tract qualifying as highly distressed. High distress designation is determined through a series of tests based on the census tract’s statistical data along with numerous other location measures. Capital Peak Partners conducts qualification analysis and can provide additional information upon request.

Qualification by Community Impact

There is no standard evaluation for community impact but this evaluation commonly focuses on the level of community impacts the transaction will provide to the low income community and/or low income persons. Methods of drawing conclusions are often subjective based on quantifiable and non-quantifiable impacts. As such, the community benefit analysis is conducted differently by each CDE lender and consequently many CDE lenders have differing minimum thresholds. Although difficult to measure, some of the quantifiable and non-quantifiable measures of community impacts include:

- Total number of direct, indirect and induced construction jobs created or maintained;

- Total number of direct, indirect and induced permanent jobs created or maintained;

- Increase of tax base for community;

- Services provided to low income persons and/or community;

- Social benefits to low income persons, non-profit organizations, community, etc;

- Level of community support;

- Renewable energy benefits;

- Job training provided.

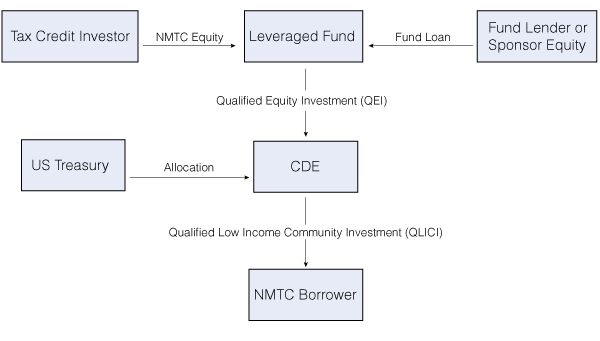

Common New Markets Tax Credit Structure

The illustration below is a very general overview of a typical NMTC structure chart identifying the general parties and their roles in the transaction.